Owning a home is now easier than ever with the Mera Ghar Mera Aashiyana Scheme. This government-backed initiative, also known as Mera Ghar Mera Aashiyana, is designed to help low- and middle-income citizens transition from renting to owning. By offering subsidized markup rates and flexible terms, the Scheme is transforming the real estate landscape for first-time buyers across Pakistan.

Key Features of the Scheme

The Mera Ghar Scheme stands out due to its extreme affordability compared to traditional bank loans. Here are the primary benefits for applicants:

- Uniform Low Markup: Recent 2025-2026 updates have introduced a flat 5% markup rate for the first 10 years of the loan.

- High Financing Limit: Eligible individuals can now secure financing for up to PKR 1 Crore (10 Million).

- Small Down Payment: You only need to provide 10% equity, as the scheme covers up to 90% of the property value.

- Extended Tenure: Pay back your loan over a period of up to 20 years to keep your monthly costs low.

- No Hidden Costs: There are no processing fees or penalties for early repayment.

Eligibility for the Mera Ghar Scheme

To qualify for the Scheme, you must meet specific criteria set by the State Bank of Pakistan:

- First-Time Owner: You must not currently own any residential unit in Pakistan.

- Valid Identity: A valid CNIC is mandatory for all Pakistani citizens applying.

- Income Proof: You must have a verifiable income, whether you are salaried, self-employed, or a business owner.

- Debt-to-Income Ratio: Your monthly installment should generally not exceed 40% of your net monthly income.

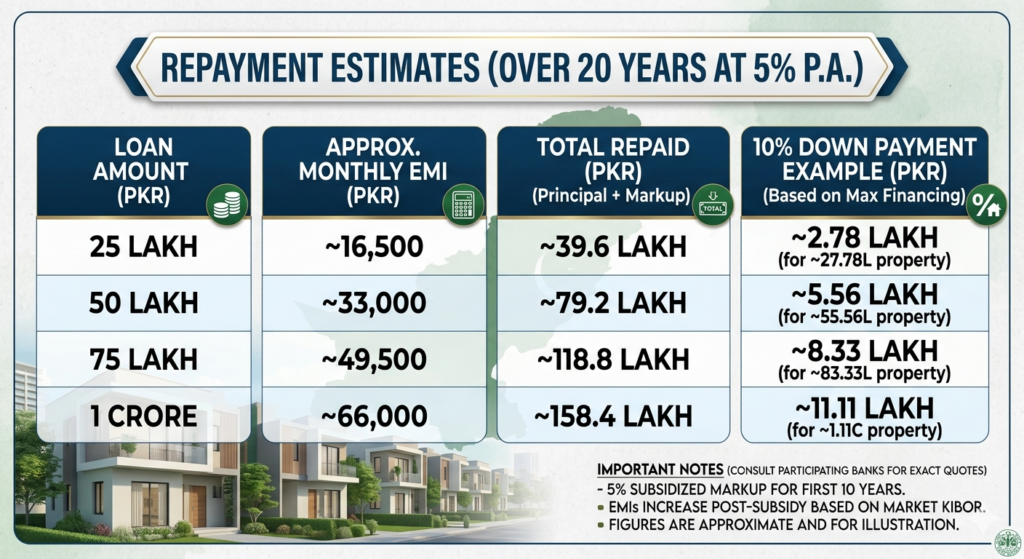

Monthly Installment Estimates

The affordability of the Mera Ghar Scheme is best seen through its monthly repayments. Below are estimates based on a 5% p.a. rate over a 20-year period:

Note: These are estimates for the first 10 years. After the subsidy period, rates typically shift to a market-based KIBOR rate.

Pros and Cons of the Mera Ghar Scheme

The Advantages

The primary benefit of the Mera Ghar Scheme is the 5% markup, which is significantly lower than standard market rates that often exceed 15%. It also encourages financial inclusivity by helping those with informal incomes through proxy assessment models.

The Challenges

While the Mera Ghar Scheme is highly beneficial, applicants should be aware that the 5% rate is fixed only for the first decade. Additionally, the strict “first-time owner” rule means you cannot use this facility if you already have property in your name.

How to Apply Today Mera Ghar Scheme

Starting your journey with the Scheme is simple. Visit any participating bank, such as NBP, HBL, or Meezan Bank, to start your application.

By choosing the Scheme, you are making a secure investment in your family’s future. Don’t wait—subsidized housing is just an application away!

Quick Summary of Key Facts

- Subsidized Rate: 5% flat markup for the first 10 years.

- Maximum Loan: Up to PKR 1 Crore (10 Million).

- Down Payment: Only 10% equity required from the borrower.

- Tenure: Up to 20 years for easy repayment.

- Eligibility: Pakistani citizens with a valid CNIC who are first-time homeowners.

Join us on Social Media

Share this Page

Subscribe